Money buys coverage. The right policy buys breathing room. Comparing insurance isn’t just a spreadsheet exercise it’s choosing how you’ll feel on the worst day: frantic and exposed, or prepared and steady. This guide cuts through jargon, shows you what actually matters, and gives you a concrete way to pick the best-value policy for your life not the most expensive, not the flashiest, but the one that holds when you need it.

Insurance basics that shape value

Before you compare quotes, get fluent in the levers that change price and protection. These terms appear across most policy types (health, auto, home/renters, life, travel, pet, business).

- Premium: What you pay to keep the policy active. Lower premiums usually mean higher out-of-pocket costs later.

- Deductible: What you pay before coverage kicks in. Annual vs. per-claim deductibles change how costs stack over time.

- Co-pay or coinsurance: Your share after the deductible. A 20% coinsurance means you pay 20% of covered costs, the insurer pays 80%.

- Coverage limits: Caps on what the insurer pays. These can be per incident, per condition, per item (sub-limits), or annual/aggregate.

- Waiting periods: Time after purchase when certain claims aren’t covered. Critical for health, pet, travel, and some property coverages.

- Exclusions: Events, conditions, or items the policy will not cover. Read this section twice—value lives here.

- Endorsements/riders: Add-ons that extend coverage (e.g., flood for property, critical illness for life).

- Network rules: For health and some specialty policies, in-network vs. out-of-network fees and access matter.

- Claim process: How you file, how fast they pay, and what documents they require. A smooth process is a hidden form of value.

- Adjusters and depreciation: For property claims, how items are valued (actual cash value vs. replacement cost) changes your outcome.

A clear comparison isn’t about chasing the lowest premium. It’s aligning these levers to your risk profile, your cash flow, and your tolerance for surprise.

Define your needs before comparing

Policies protect risks. You can’t rank them well until you name your real risks and constraints.

- Your biggest exposures:

- Health/medical: Chronic conditions, maternity plans, access to specialists.

- Vehicle use: Daily commuting, high-traffic routes, ridesharing, new or financed car.

- Home/renters: Flood risk, theft rates, valuables, building age, security.

- Life: Income replacement, debts, dependents, time horizon.

- Travel: Nonrefundable bookings, medical evacuation needs, trip frequency.

- Pet: Breed-specific conditions, age, chronic care needs.

- Business: Liability, professional errors, cyber risk, stock/inventory.

- Your budget reality:

- Monthly affordability: What you can pay consistently without strain.

- Emergency cash: What you could cover in a crisis before reimbursement.

- Debt/obligations: Loans or responsibilities that must be protected.

- Your care preferences:

- Provider choice: Do you need open networks or are you okay with a restricted panel?

- Speed vs. savings: Higher deductibles lower premiums but require more cash up front.

- Service expectations: 24/7 support, local agents, app-based claims.

- Legal/contractual requirements:

- Mandates: Minimum auto liability, mortgage-required homeowners coverage, visa-required travel insurance, business client contracts.

Knowing these inputs lets you filter policies fast and avoid “shiny object” features you’ll never use.

The essential components to compare

When you ask for quotes or open sample policy documents, anchor your comparison on these elements.

- Coverage scope:

- Named perils vs. all-risk: All-risk covers everything not excluded; named perils covers only listed events.

- Primary inclusions: Liability, property damage, medical, loss-of-use, specialty protections (flood, earthquake, cyber, rental car, evacuation).

- Sub-limits: Jewelry, electronics, cash, alternative therapies, specialty equipment.

- Financial structure:

- Deductible type and amount: Annual vs. per-incident vs. per-condition.

- Coinsurance/co-pay: After deductible, what’s your ongoing share?

- Limits: Per-claim, per-condition, per-item, annual, lifetime.

- Exclusions and conditions:

- Fine print: Wear and tear, pre-existing conditions, “acts of God,” war/civil unrest, professional use exclusions.

- Documentation requirements: Inspections, appraisals, maintenance records, medical history.

- Claims experience:

- Process: App, phone, email, portal; required documentation; pre-authorization rules.

- Timelines: Typical payout speed; emergency advances.

- Dispute resolution: Appeals, ombudsman, arbitration.

- Price stability:

- Rate change triggers: Age bands, claims history, location shifts, inflation adjustments.

- No-claims benefits: Discounts, cashback, vanishing deductibles.

- Service and reputation:

- Support: 24/7 claims line, multilingual assistance, local agents.

- Reviews: Look for recent claims-specific feedback, not just sales experiences.

Create a short list of must-haves and deal-breakers for each category. If a policy fails a deal-breaker (e.g., excludes flood in a flood-prone zone), remove it regardless of price.

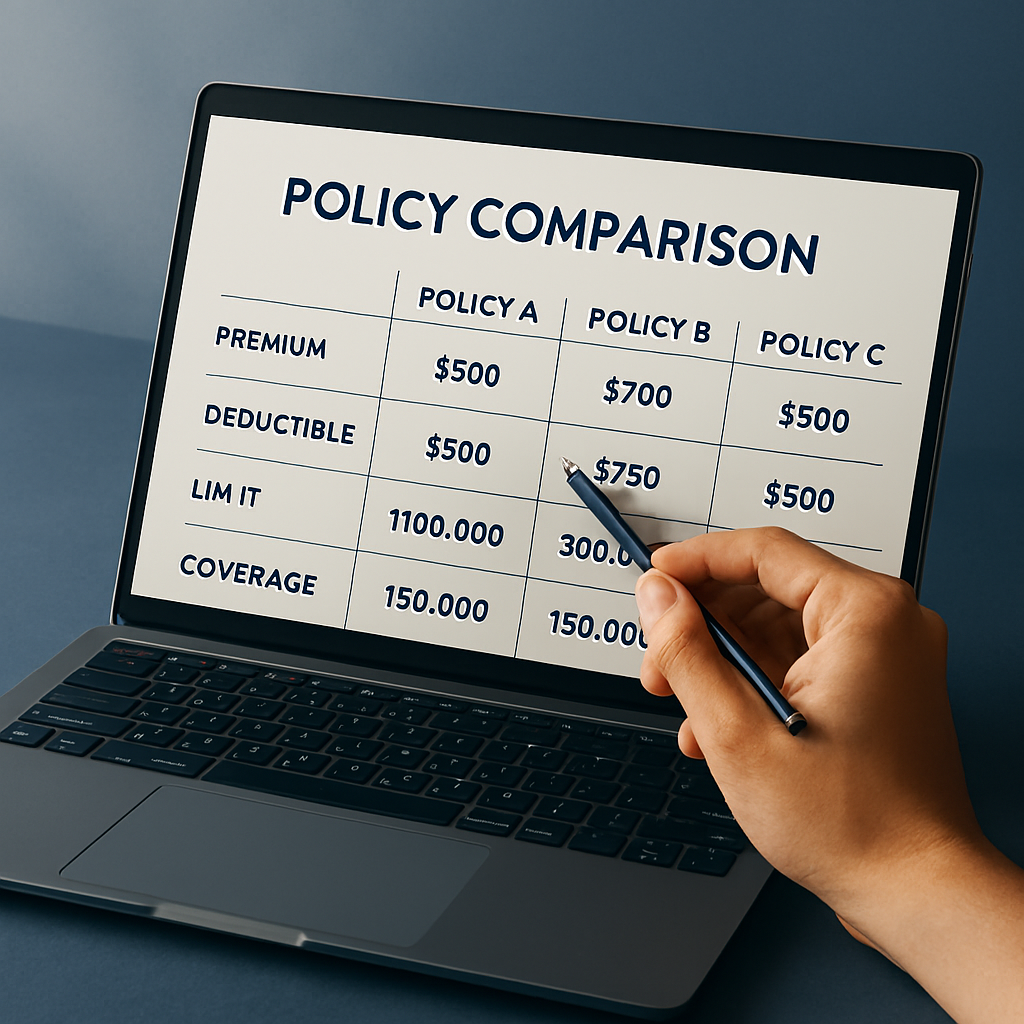

A simple framework to compare policies side by side

Use a one-page grid for apples-to-apples evaluation. Keep it lean and focused on decisions.

| Attribute | Policy A | Policy B | Policy C |

| Coverage type/scope | |||

| Deductible (type/amount) | |||

| Coinsurance/co-pay | |||

| Key limits (per-claim/annual) | |||

| Notable sub-limits | |||

| Top exclusions | |||

| Claim process & timeline | |||

| Price today | |||

| Expected price changes | |||

| Standout benefit | |||

| Red flag |

Tip: Weight what matters most to you (e.g., coverage scope = 40%, price = 25%, service = 20%, exclusions = 15%). Multiply each policy’s 1–5 rating by the weight to pick the best value, not just the cheapest.

Coverage deep-dive by policy type

Each category has its own “make-or-break” details. Here’s what to prioritize so you don’t overpay or under-protect.

Health insurance (individual/family)

- Network access:

- Lead doctor or free choice: Need referrals? Is your preferred hospital in-network?

- Emergency care: Out-of-network emergency rules and cost-sharing.

- Cost-sharing:

- Deductible and out-of-pocket maximum: Your worst-case annual spend matters more than the premium.

- Drug tiers: Formularies, prior authorization, and specialty medication caps.

- Benefits depth:

- Inclusions: Inpatient, outpatient, maternity, mental health, rehab, preventive care.

- Exclusions and caps: Alternative therapies, devices, dental/vision, fertility.

- Chronic care and pre-authorization:

- Case management: Support for long-term conditions.

- Pre-auth rules: For imaging, surgeries, and high-cost drugs.

Auto insurance

- Liability limits:

- Bodily injury/property damage: Minimums rarely suffice; choose limits that match your assets and risk.

- Your car’s protection:

- Collision/comprehensive: Weather, theft, vandalism, animal strikes.

- Deductible balance: Higher deductibles cut premiums but can sting after an accident.

- Extras that matter:

- Uninsured/underinsured motorist: Crucial in areas with low insurance rates.

- Medical payments/personal injury protection: Covers you and passengers.

- Rental and roadside: Budget-friendly add-ons with outsized convenience.

- Usage and discounts:

- Telematics/usage-based: Can reduce premiums if you drive safely.

- Multi-policy/multi-vehicle: Stacking discounts improves value.

Homeowners/renters insurance

- Valuation method:

- Replacement cost vs. actual cash value: Replacement cost avoids depreciation losses on claims.

- Perils and gaps:

- All-risk vs. named peril: All-risk is broader, exclusions still apply.

- Flood/earthquake: Usually excluded; may require separate policies.

- Sub-limits to watch:

- Valuables: Jewelry, watches, art, instruments, and electronics need riders/appraisals.

- Business equipment: Often capped; consider endorsements if you work from home.

- Loss of use and liability:

- Temporary housing: Adequate daily limits and duration.

- Personal liability: Coverage for injuries on your property or damage you cause elsewhere.

Life insurance

- Term vs. whole:

- Term: Higher coverage for lower cost, fixed period.

- Whole/universal: Lifetime coverage with cash value; more complex and expensive.

- Coverage amount:

- Rule of thumb: 10–15× annual income, plus debts and education goals.

- Needs-based: Income, dependents, mortgage, caregiving costs, funeral.

- Underwriting and riders:

- Medical exams: Fully underwritten often yields better pricing.

- Riders: Waiver of premium, accelerated death benefit, child term, critical illness.

Travel insurance

- Trip costs vs. medical:

- Trip cancellation/interruption: Match nonrefundable amounts.

- Medical and evacuation: Prioritize high limits and reliable assistance networks.

- Coverage triggers and exclusions:

- Named reasons: Illness, severe weather, job loss; “cancel for any reason” is pricier but flexible.

- Adventure sports: Many exclude high-risk activities without a rider.

Pet insurance

- Accident & illness vs. accident-only:

- Illness coverage: Worth it for chronic/cancer risks; accident-only is budget-friendly.

- Waiting periods: Orthopedic waiting often longer.

- Financial settings:

- Annual vs. per-condition deductibles: Impacts multi-condition years.

- Limits and reimbursement: Aim for strong coverage where your pet’s breed is vulnerable.

Business insurance (brief)

- Core:

- General liability, professional liability (E&O), property, cyber, workers’ comp.

- Contracts: Clients may require specific limits or endorsements.

- Key levers:

- Claims-made vs. occurrence: Especially for professional liability—know retroactive dates and tail coverage.

- Business interruption: Clear triggers, realistic income calculations, and indemnity periods.

Red flags and fine-print traps

- Vague exclusions:

- Red flag: “Wear and tear” or “pre-existing” without definitions.

- Fix: Look for clear definitions and examples.

- Bilateral or related-condition clauses:

- Impact: One-side injury makes the other side ineligible later (common in pet/health).

- Fix: Check how “related” is defined.

- Depreciation without replacement option:

- Impact: You receive less than the cost to buy new.

- Fix: Choose replacement cost where possible.

- Low sub-limits on high-value items:

- Impact: Jewelry/electronics payouts cap out fast.

- Fix: Add scheduled coverage with appraisals.

- Mandatory arbitration with limited appeals:

- Impact: Harder to contest denied claims.

- Fix: Prefer transparent appeal pathways.

- Short reporting windows:

- Impact: Late notice can void claims.

- Fix: Know the timeline; set reminders.

- “Reasonable and customary” pricing clauses:

- Impact: Insurer can reduce payouts if they deem costs excessive.

- Fix: Ask how they calculate and whether you can pre-authorize.

Cost optimization without losing protection

- Increase deductibles strategically:

- Why: Lower premiums, maintain catastrophic protection.

- How: Set a deductible equal to your emergency fund comfort.

- Bundle policies:

- Why: Multi-policy discounts.

- How: Home + auto, or business + cyber with same carrier.

- Adjust coverage to reality:

- Why: Avoid paying for risks you don’t have.

- How: Drop collision on an older car; add flood if you’re in a flood zone.

- Improve your risk profile:

- Why: Discounts and fewer claims.

- How: Security systems, safe driving programs, wellness screenings.

- Pay annually when possible:

- Why: Avoid installment fees and sometimes get a discount.

- How: Budget monthly into a sinking fund, then pay in a lump sum.

- Review yearly:

- Why: Life changes, so should coverage.

- How: New address, dependents, income, or valuables = policy update.

Real-world value: quick scenarios and math

Seeing the numbers clarifies trade-offs. These examples use round figures to illustrate structure. Your actual quotes will differ.

- Homeowners: replacement cost vs. actual cash value (ACV):

- Scenario: A laptop originally bought for 1,200 is stolen; replacement now costs 1,300. Depreciation is 40%, deductible is 250.

- ACV payout:

Payout=(1,200×(1−0.40))−250=720−250=470\text{Payout} = (1{,}200 \times (1 – 0.40)) – 250 = 720 – 250 = 470

- Replacement cost payout:

Payout=1,300−250=1,050\text{Payout} = 1{,}300 – 250 = 1{,}050

- Takeaway: Replacement cost can be worth the extra premium for meaningful items.

- Auto: deductible decision:

- Scenario: Comprehensive claim for windshield and bodywork totals 1,800. Compare 250 vs. 1,000 deductibles.

- Out-of-pocket at 250 deductible:

250250

- Out-of-pocket at 1,000 deductible:

1,0001{,}000

- If the higher deductible saves 180/year in premium, breakeven is:

1,000−250180≈4.17 years\frac{1{,}000 – 250}{180} \approx 4.17 \text{ years}

- Takeaway: If you expect a claim within ~4 years or value lower shock costs, choose the lower deductible.

- Health: out-of-pocket maximum (OOPM) as a safety net:

- Scenario: High-cost year with multiple procedures totaling 30,000. Plan A: lower premium, OOPM 7,500. Plan B: higher premium, OOPM 4,000.

- Worst-case spend Plan A:

OOPM=7,500\text{OOPM} = 7{,}500

- Worst-case spend Plan B:

OOPM=4,000\text{OOPM} = 4{,}000

- Premium difference 70/month = 840/year; if a high-cost year hits, Plan B can net-save:

7,500−4,000−840=2,6607{,}500 – 4{,}000 – 840 = 2{,}660

- Takeaway: In risky years, lower OOPM plans can win even with higher premiums.

- Pet: coinsurance effect:

- Scenario: Eligible surgery costs 2,400; deductible 300. Compare 70% vs. 90% reimbursement.

- At 70% reimbursement:

Your cost=300+0.30×(2,400−300)=300+630=930\text{Your cost} = 300 + 0.30 \times (2{,}400 – 300) = 300 + 630 = 930

- At 90% reimbursement:

Your cost=300+0.10×(2,400−300)=300+210=510\text{Your cost} = 300 + 0.10 \times (2{,}400 – 300) = 300 + 210 = 510

- Takeaway: Higher reimbursement shines on big claims; worth it if premiums aren’t significantly higher.

A step-by-step process to pick the best value

- List your real risks and priorities.

- Label: Health access, liability protection, asset replacement, cash-flow smoothing.

- Set your budget bands.

- Label: Monthly premium target, maximum out-of-pocket per claim, and per year.

- Collect 3–4 comparable quotes.

- Label: Same coverage types and limits to avoid apples-to-oranges.

- Read the exclusions first.

- Label: Remove policies that exclude your most likely claims.

- Map financials in a grid.

- Label: Deductible, coinsurance, limits, sub-limits, OOPM (health), depreciation rules (property).

- Pressure-test with two scenarios.

- Label: One minor claim and one catastrophic claim. Calculate your total cost under each.

- Score by weighted priorities.

- Label: Assign weights and pick the highest total, not just lowest premium.

- Verify service and stability.

- Label: Claims timelines, complaints, rate-change patterns.

- Ask for clarifications in writing.

- Label: Ambiguous clauses, pre-authorization needs, valuation methods.

- Bind coverage and set reminders.

- Label: Renewal review at least 30 days before expiration.

FAQs

- Is the cheapest policy ever the best value? Sometimes, if your risks are low and exclusions don’t touch your likely claims. But value is the ratio of protection you’ll actually use to the price you pay—check limits, sub-limits, and claims reputation.

- How many quotes should I compare? Three to four is the sweet spot: enough to see variation, not so many you drown in paperwork.

- What’s the most overlooked line item? Sub-limits. They quietly cap your payout for the very items you care about most—jewelry, electronics, specialty equipment.

- Can I switch insurers easily? Yes, but time it before renewals and check how pre-existing conditions or in-progress claims will be treated. For liability or claims-made policies, watch retroactive dates.

- How often should I review coverage? Annually, and after big life changes: new address, new job, marriage, dependents, major purchases, or renovations.

- What documents speed up claims? Photos, receipts, appraisals, police reports, medical notes, service logs, and any pre-authorization approvals.

Copy-and-use checklist

- Define risks: Health, property, liability, income, travel.

- Set budget: Monthly premium, per-claim cash, annual worst-case.

- Shortlist 3–4 carriers: Matching coverage specs.

- Read exclusions: Eliminate mismatches early.

- Compare financials: Deductible, coinsurance, limits, sub-limits.

- Check valuation: Replacement cost vs. ACV.

- Confirm claims: Process, timeline, documents.

- Test scenarios: Minor and major claims math.

- Score and choose: Weighted priorities.

- Calendar renewal: Review and adjust.

Откройте для себя незабываемые моменты на море с арендой яхты в Сочи|арендой яхт в Сочи|прокатом яхт в Сочи|арендой яхт|яхтами в Сочи|снять яхту в Сочи|яхта в Сочи аренда|сочи аренда яхт|яхты аренда|яхты Сочи!

Аренда яхты привлекает все большее количество людей, желающих ощутить свободу на воде. Это не удивительно, ведь яхта открывает новые горизонты и возможности для путешествий. На борту яхты вы сможете насладиться красотой природы и моментами уединения.

Аренда яхты предоставляет высокий уровень комфорта и удобства. На яхте есть все необходимое для приятного времяпрепровождения, включая просторные каюты, кухню и зоны для отдыха. Существуют разные классы яхт, что позволяет удовлетворить любые запросы клиентов.

Многие ошибочно считают, что аренда яхты — это привилегия только обеспеченных клиентов. На сегодня существует множество компаний, предлагающих яхты по разным ценовым категориям. Вам не обязательно быть миллионером, чтобы провести время на шикарной яхте.

При аренде яхты важно придерживаться правил безопасности на воде. Убедитесь, что яхта полностью исправна и оборудована всеми необходимыми средствами безопасности. Также стоит изучить условия аренды, чтобы избежать неприятных ситуаций.

Откройте для себя незабываемые моменты на море с арендой яхты в Сочи|арендой яхт в Сочи|прокатом яхт в Сочи|арендой яхт|яхтами в Сочи|снять яхту в Сочи|яхта в Сочи аренда|сочи аренда яхт|яхты аренда|яхты Сочи!

Аренда яхты становится все более популярной среди любителей активного отдыха. Это не удивительно, ведь яхта открывает новые горизонты и возможности для путешествий. Путешествие по морю на яхте — это возможность увидеть мир с другой стороны.

Одним из основных преимуществ аренды яхт является комфорт. На яхте есть все необходимое для приятного времяпрепровождения, включая просторные каюты, кухню и зоны для отдыха. Вы можете выбрать яхту в зависимости от своих требований и количества человек в компании.

Аренда яхты — это не только для богатых людей, как многие думают. На сегодня существует множество компаний, предлагающих яхты по разным ценовым категориям. Таким образом, каждый может позволить себе провести время на воде, наслаждаясь отдыхом.

Безопасность — важный аспект при аренде яхты, который нельзя игнорировать. Убедитесь, что яхта полностью исправна и оборудована всеми необходимыми средствами безопасности. Также стоит изучить условия аренды, чтобы избежать неприятных ситуаций.

Откройте для себя незабываемые моменты на море с арендой яхты в Сочи|арендой яхт в Сочи|прокатом яхт в Сочи|арендой яхт|яхтами в Сочи|снять яхту в Сочи|яхта в Сочи аренда|сочи аренда яхт|яхты аренда|яхты Сочи!

Аренда яхты привлекает все большее количество людей, желающих ощутить свободу на воде. Это не удивительно, ведь яхта открывает новые горизонты и возможности для путешествий. Путешествие по морю на яхте — это возможность увидеть мир с другой стороны.

Аренда яхты предоставляет высокий уровень комфорта и удобства. На яхте есть все необходимое для приятного времяпрепровождения, включая просторные каюты, кухню и зоны для отдыха. Вы можете выбрать яхту в зависимости от своих требований и количества человек в компании.

Стоит отметить, что аренда яхты может быть доступна каждому. На сегодня существует множество компаний, предлагающих яхты по разным ценовым категориям. Таким образом, каждый может позволить себе провести время на воде, наслаждаясь отдыхом.

Не забывайте о безопасном подходе к аренде яхты. Убедитесь, что яхта полностью исправна и оборудована всеми необходимыми средствами безопасности. Знайте свои права и обязанности, чтобы аренда яхты прошла без осложнений.

Мотоцикл модели jhl — это. мощность и скорость. Что сразу же привлекает внимание — с использованием качественных материалов.

Второй важный аспект — это надежность. Модель jhl проверена временем и демонстрирует высокие показатели. Пользователи отмечают, что все детали работают без сбоев.

Третий аспект — это. Он позволяет мотоциклу развивать высокую скорость. Двигатель этого мотоцикла легко адаптируется. Это делает его идеальным.

Наконец, стоит отметить — это цена. jhl предлагает отличное соотношение цены и качества. Учитывая все его преимущества, он доступен для широкой аудитории. Таким образом, jhl — это.

jhl https://jhl/

На сайте rubber stamp maker online|stamp making online|rubber stamp online maker|stamp maker|online stamp maker|stamp maker online|stamp creator online|make a stamp online|make stamp online|online stamp design maker|make stamps online|stamps maker|online stamp creator|stamp online maker|stamp online maker free|stamp maker online free|create stamp online free|stamp creator online free|online stamp maker free|free online stamp maker|free stamp maker online|make stamp online free you can create and order the stamps you need quickly and efficiently.

that provides a platform for crafting unique and professional-looking stamps. With this innovative technology, individuals can make personalized stamps that reflect their brand or personality. The process involves selecting a template, adding text or images, and choosing the stamp size and material .

The benefits of using a rubber stamp maker online involve the ability to design and order stamps from anywhere with an internet connection . Additionally, the online platform provides a wide range of templates and design options . This makes it a great option for those who want to add a personal touch to their documents .

Features of Rubber Stamp Maker Online

The rubber stamp maker online provides an array of tools and options that cater to different needs and preferences . One of the key features is the capability to add images and graphics to the stamp design. This makes it possible for individuals to add a touch of creativity to their stamps.

Another feature is the option to select from various stamp sizes and shapes . This provides users with the flexibility to choose the best option for their needs . Furthermore, the online platform offers a preview feature that allows users to see their design before ordering .

Benefits of Using Rubber Stamp Maker Online

Using a rubber stamp maker online has several perks, including the ability to create custom stamps quickly and easily. One of the main benefits is the option to design and order stamps at any time . This reduces the need for physical visits to a stamp-making store .

Another benefit is the option to choose from various fonts, colors, and images. This allows businesses to incorporate their brand identity into the stamps . Additionally, the online platform provides a cost-effective solution for creating custom stamps .

Conclusion and Future of Rubber Stamp Maker Online

In conclusion, the rubber stamp maker online is a innovative platform that offers a wide range of design options and features. The future of rubber stamp maker online looks promising, with advancements in technology and design . As the demand for custom stamps continues to grow , the rubber stamp maker online will remain a popular choice for those seeking a convenient and efficient way to make personalized stamps.

The potential applications range from business and marketing to art and crafts . As the user base grows and becomes more diverse, the rubber stamp maker online will remain at the forefront of the custom stamp-making industry. Whether an individual seeking to add a personal touch to your documents , the rubber stamp maker online is an excellent choice .

Create your perfect online print in just a few clicks with rubber stamp maker online, stamp making online, rubber stamp online maker, stamp maker, online stamp maker, stamp maker online, stamp creator online, make a stamp online, make stamp online, online stamp design maker, make stamps online, stamps maker, online stamp creator, stamp online maker, stamp online maker free, stamp maker online free, create stamp online free, stamp creator online free, online stamp maker free, free online stamp maker, free stamp maker online, make stamp online free — fast, easy and free!

Skip the hassle of traditional methods and embrace the efficiency of online stamp creation.

Benefits of Using an Online Rubber Stamp Maker

Save money and get your stamp produced swiftly with these reliable online services.

Steps to Create a Rubber Stamp Online

The initial step is choosing a trustworthy online platform with an intuitive design interface.

Choosing the Right Rubber Stamp Maker

Assess reliability and design features by carefully inspecting online reviews and pricing structures.

Если вы хотите найти подходящий вариант для своей машины и при этом сэкономить, тогда стоит зимние шины купить|зимние шины спб|купить зимние шины спб|зимние шины в спб|купить зимние шины в спб|зимняя резина спб купить|зимняя резина в спб купить|купить шины зима|зимние колёса купить|петербург зимние шины|шины зимние в петербурге|шины зимние в санкт петербурге|купить зимние шины недорого|купить недорогие зимние шины|зимняя резина дешево|купить дешево зимнюю резину|купить автошины зимние|шины зимние со склада|купить зимнюю резину в спб недорого|комплект зимней резины купить|продажа зимних шин в спб, поскольку это позволит вам выбрать лучшее качество по оптимальной цене.

Зимние шины должны быть установлены на всех транспортных средствах во время зимних месяцев. При правильном выборе зимних шин можно значительно снизить риск аварий и улучшить сцепление с дорогой Зимние шины обеспечивают лучшее сцепление с дорогой и могут спасти вас от аварий . Кроме того, зимние шины могут улучшить управляемость транспортного средства и снизить риск заноса Зимние шины обеспечивают лучшую стабильность и могут снизить риск аварий на прямых участках дороги .

Зимние шины также могут снизить риск повреждения транспортного средства и других объектов на дороге Зимние шины могут снизить риск повреждения транспортного средства и других объектов на дороге . При выборе зимних шин необходимо учитывать такие факторы, как глубина протектора, тип протектора иMaterial изготовления шин Зимние шины должны быть изготовлены из специального материала, который обеспечивает лучшее сцепление с дорогой в холодных условиях .

Типы зимних шин

Существует несколько типов зимних шин, каждый из которых имеет свои преимущества и недостатки Существует несколько категорий зимних шин, каждый из которых имеет свои преимущества и недостатки. Например, стudded шины имеют металлические шипы, которые обеспечивают лучшее сцепление с дорогой на льду Studded шины имеют специальную конструкцию, которая обеспечивает лучшее сцепление с дорогой в холодных условиях . Однако, такие шины могут быть запрещены в некоторых регионах из-за повреждения дорожного покрытия Studded шины могут быть запрещены в некоторых регионах из-за повреждения дорожного покрытия .

Другой тип зимних шин – studless шины, которые не имеют металлических шипов Studless шины не имеют металлических шипов, но обеспечивают лучшее сцепление с дорогой на мокрых поверхностях. Такие шины более тихие и комфортные, чем studded шины, но могут быть менее эффективными на льду Studless шины имеют лучшую износостойкость, чем studded шины, но могут быть менее эффективными на льду.

Как выбрать зимние шины

При выборе зимних шин необходимо учитывать несколько факторов, включая тип транспортного средства, условия вождения и личные предпочтения При выборе зимних шин необходимо учитывать тип транспортного средства, условия вождения и личные предпочтения . Например, если вы живете в регионе с сильными снегопадами, вам может потребоваться более агрессивный тип шин Если вы живете в регионе с сильными снегопадами, вам может потребоваться более глубокий протектор .

Кроме того, необходимо учитывать размер шин и тип шин, которые подходят вашему транспортному средству Необходимо учитывать такие факторы, как размер шин, тип шин и производитель . Также важно прочитать отзывы и сравнить цены разных производителей Также необходимо проверить гарантию и сравнить цены разных производителей.

Где купить зимние шины

Зимние шины можно купить в различных магазинах и интернет-магазинах Зимние шины можно найти в различных торговых центрах и интернет-магазинах. Например, можно посетить магазины, такие как ОЗОН, Wildberries или Авторусь Можно посетить интернет-магазины, такие как Яндекс.Маркет или Google Маркет . Также можно проверить официальные сайты производителей, такие как Michelin, Continental или Nokian Также можно посетить сайты дилеров, такие как Toyota или Ford .

При покупке зимних шин необходимо проверить качество и соответствие шин вашему транспортному средству При покупке зимних шин необходимо проверить цены и качество шин. Кроме того, необходимо учитывать такие факторы, как доставка и установка шин Необходимо учитывать такие факторы, как доставка и установка шин .

Для обеспечения безопасности во время зимней езды многие автомобилисты предпочитают использовать нешипованные зимние шины|зимние нешипованные шины|купить зимние нешипованные шины|шины липучки зимние купить в спб|шины липучки зимние купить|купить зимние липучки|зимняя резина липучка купить|колеса зимние липучка купить|нешипованная зимняя резина|купить нешипованную зимнюю резину|недорогая нешипованная зимняя резина|зимние шины без шипов купить|купить зимнюю резину без шипов|шины липучка купить в спб|шины липучка купить|шины зима липучка купить|резина липучка купить в спб|резина липучка купить|колеса липучка купить|зима липучка купить|покрышки липучки купить|зимние нешипуемые шины, которые обеспечивают оптимальное сцепление на льду и снегу без необходимости шипов.

являются современным аналогом шипованных шин, предназначенных для обеспечения лучшего сцепления с дорогой в зимних условиях. Они созданы для того, чтобы обеспечить оптимальный уровень сцепления с дорогой в различных зимних условиях, включая снег, лёд и мокрый асфальт . Эти шины имеют специальную резиновую смесь, которая обеспечивает отличное сцепление с поверхностью, не требуя дополнительных конструктивных элементов .

Нешипованные зимние шины получили широкое распространение в последние годы благодаря своим уникальным свойствам и преимуществам . Они обеспечивают превосходную тягу и сцепление на снегу и льду, что делает их идеальным выбором для регионов с суровыми зимами .

Преимущества нешипованных зимних шин

Нешипованные зимние шины характеризуются отсутствием металлических шипов, что снижает риск повреждения дорожного покрытия и обеспечивает более тихую езду. Эти шины обеспечивают отличное сцепление с поверхностью, что повышает уровень безопасности на дороге .

Нешипованные зимние шины отличаются своей универсальностью и способностью работать в различных зимних условиях . Они обеспечивают превосходную тягу и сцепление на снегу и льду, что делает их идеальным выбором для регионов с суровыми зимами .

Характеристики нешипованных зимних шин

Нешипованные зимние шины характеризуются наличием специальных канавок и протекторов, которые улучшают водоотвод и предотвращают аквапланирование . Эти шины разработаны с использованием современных технологий и материалов, что делает их высокоэффективными и долговечными.

Нешипованные зимние шины отличаются своей способностью работать в различных зимних условиях, включая снег, лёд и мокрый асфальт . Они предназначены для использования в районах, где шипованные шины запрещены или не рекомендуются из-за потенциального вреда дорожному покрытию.

Выбор нешипованных зимних шин

Нешипованные зимние шины имеют ряд достоинств, среди которых отсутствие шипов, что делает их более подходящими для городских условий эксплуатации . Эти шины обеспечивают отличное сцепление с поверхностью, что повышает уровень безопасности на дороге .

Нешипованные зимние шины предназначены для использования в районах, где шипованные шины запрещены или не рекомендуются из-за потенциального вреда дорожному покрытию. Они разработаны с использованием современных технологий и материалов, что делает их высокоэффективными и долговечными .

Если вам нужны качественные услуги [url=https://kliningovaya-kompaniya-01.ru/]клининг|клининг в москве|клининг москва|клининговая компания|клининговая компания в москве|клининговая компания москва|заказать клининг|клининговая служба|клининг москва уборка|услуги клининга|услуги клининга в москве цены на услуги|клининг мск|клининг компании в москве|клининг уборка|заказать клининг в москве|клининг в москве цена|клининг компания|сайт клининговой компании|сайт клининга[/url], мы готовы предложить вам лучшее решение!

Клининг включает в себя множество различных услуг, от уборки до профессиональной мойки окон.

If you are looking for an experienced [url=https://sedenko.net/next-js-developer]next.js developer|next js developer|next developer|next developer freelancer|next freelancer|next js freelancer|hire next.js developer|freelance next.js developer|remote next.js developer|next.js full-stack developer|next.js developer for hire|custom next.js development|next.js website developer|next.js expert freelancer|next.js web app developer|next.js ssr developer|next.js seo expert|next.js performance optimization|next.js developer portfolio|next.js development services|next.js developer available|hire freelance next.js developer|experienced next.js developer|next.js + react developer|full-time next.js freelancer[/url],who can create a high-performance and scalable website using Next.js technology, you can find the right specialist offering a wide range of development services on this platform.

Next.js is a versatile tool for creating fast and scalable web applications . With its ability to handle server-side rendering and static site generation, it has become a go-to choice for developers looking to create fast and efficient web applications. there is a growing need for professionals who can develop high-quality web applications using Next.js.

learning Next.js has become a top priority for web developers . With the right skills and knowledge, developers can create complex web applications with ease . Next.js developers are in high demand, and they have a wide range of job opportunities available to them.

Key Skills for Next.js Developers

To become a successful Next.js developer, one needs to have a solid grasp of programming concepts and experience with Next.js. This includes proficiency in JavaScript and React, as well as knowledge of HTML, CSS, and other front-end development tools . A good Next.js developer should also have strong analytical and critical thinking skills .

In addition to technical skills, Next.js developers should be able to stay up-to-date with the latest developments and advancements in the field. This includes knowledge of testing and debugging techniques. By possessing these skills and knowledge, Next.js developers can build fast and scalable websites that provide a great user experience .

Next.js Developer Job Responsibilities

the role of a Next.js developer involves a range of tasks and activities . This includes creating fast and scalable web applications using Next.js . Next.js developers are also responsible for troubleshooting and debugging issues .

In addition to these technical tasks, Next.js developers may also be involved in collaborating with cross-functional teams . They may also be responsible for participating in online communities and forums. By fulfilling these responsibilities, Next.js developers can build fast and scalable websites that provide a great user experience .

Future of Next.js Development

The future of Next.js development looks bright, with a wide range of job opportunities available for Next.js professionals. As the web development landscape continues to evolve, Next.js will remain a versatile tool for creating complex web projects. With its ability to handle server-side rendering and static site generation, Next.js is well-positioned to meet the needs of modern web development .

As a result, companies will continue to look for experts who can leverage the power of Next.js. By acquiring Next.js skills and knowledge, developers can position themselves for success in the web development industry . With the right skills and knowledge, developers can take advantage of the many job opportunities available for Next.js professionals .

Visit [url=https://hdizlefilm.site]full hd film izle 4k|film izle 4k|kirpi sonic resmi|4k film izle|full film izle 4k|4k filmizle|hd film izle|turkce dublaj filmler 4k|film izle turkce|romulus turkce dublaj izle|filmizle 4k|4 k film izle|4k f?lm ?zle|4k turkce dublaj filmler|k?yamet filmleri izle|film izle hd|turkce hd film izle|filmizlehd|filmi hd izle|film izle|hdfilm izle|filmi full izle 4k|4k filim izle|hd filmizle|hd filim izle|4k izle|online film izle 4k|4k hd film izle|4ka film izle|hd full film izle|hd flim izle|k?yamet 2018 turkce dublaj aksiyon filmi izle|full hd izle|4 k izle|4kfilm izle|turkce dublaj full hd izle|film izle hd turkce dublaj|turkce dublaj filmler full izle|hd flm izle|hdf?lm ?zle|4k flim izle|hd izle|hd turkce dublaj izle|s?k?ysa yakala|hd film izle turkce dublaj|4k izle film|sonsuz s?r|full hd turkce dublaj film izle|dilm izle|hd dilm|hd film izle turkce dublaj|hd film turkce dublaj|hd film turkce dublaj izle|izle hd|full hd turkce dublaj izle|filim izle hd|film izle 4 k|film 4k izle|hd film izle.|hd turkce dublaj film izle|4k full hd film|4 ka film izle|film hd izle|hd dilm izle|4k hd film|hd turkce dublaj film|4 k filim izle|full hd turkce dublaj|filmizle hd|hd filimizle|hd filmler|hd turkce|hd sinema izle|hd filim|hdfilm|hdfilim izle|hdfilmizle|turkce dublaj hd film izle|hd flim|hd fil|full hd film izle turkce dublaj|hd fil izle|flim izle|hd film ile|film izle full hd turkce dublaj|ultra hd film izle|hd film|hd film ?zle|hd film ize|full izle|hd film.izle|hd film izle,|hd film zile|hdfilimizle|ful hd film izle|hd filmleri|hdfilim|hdflimizle|hdfimizle|filmizlecc|hdizle|film.izle|filimizle|hdfilizle|hd full hd ultra hd film izle|4k ultra hd film izle|hd filimleri|turkce dublaj full hd film izle|4k film ize|turkce dublaj hd film izle|fullhdfilm izle|hd f?l?m ?zle|hd film ilze|hd turkce dublaj|full izle 4k[/url], to watch full movies in high quality.

As the demand for high-quality content continues to grow, the development of Full HD film izle 4K technology is becoming increasingly important for the film industry.

Benefits of Watching Full HD Film Izle 4K

Whether it’s the roar of the crowd in a sports movie or the quiet whispers of a romantic comedy, Full HD film izle 4K brings the movie to life in a way that is both captivating and engaging.

How to Watch Full HD Film Izle 4K

To get the most out of your Full HD film izle 4K experience, it’s also important to consider the quality of your internet connection and the capabilities of your device.

Conclusion and Future of Full HD Film Izle 4K

With its stunning visuals, immersive sound, and range of benefits, Full HD film izle 4K is sure to remain a popular choice for film enthusiasts around the world.

Если вы ищете [url=https://kupit-zimnie-shipovannie-shini.ru/]зимние шины шипованные|зимняя резина шипованная|резина зимняя шипованная|купить шины шипованные|купить шипованные шины|купить шипованную резину|шины зимние шипованные купить|зимняя резина шипованная купить|зимняя шипованная резина спб|шипованные шины цена|купить зимнюю шипованную резину в санкт петербурге|автошины шипованные|шипованная резина зима|автошины зимние шипованные|недорогая зимняя шипованная резина|недорогая шипованная резина|авторезина шипованная|шипованная резина новая купить|купить зимнюю резину в спб недорого шипованную|покрышки зимние шипованные купить спб[/url], у нас есть отличный выбор по доступным ценам!

Шипы на шинах увеличивают заметности автомобиля на сложных участках дороги.

Тем не менее, шипованные шины имеют и свои недостатки

Visit the site [url=https://filmlerivediziler.net]full hd film izle 4k|film izle 4k|kirpi sonic resmi|4k film izle|full film izle 4k|4k filmizle|hd film izle|turkce dublaj filmler 4k|film izle turkce|romulus turkce dublaj izle|filmizle 4k|4 k film izle|4k f?lm ?zle|4k turkce dublaj filmler|k?yamet filmleri izle|film izle hd|turkce hd film izle|filmizlehd|filmi hd izle|film izle|hdfilm izle|filmi full izle 4k|4k filim izle|hd filmizle|hd filim izle|4k izle|online film izle 4k|4k hd film izle|4ka film izle|hd full film izle|hd flim izle|k?yamet 2018 turkce dublaj aksiyon filmi izle|full hd izle|4 k izle|4kfilm izle|turkce dublaj full hd izle|film izle hd turkce dublaj|turkce dublaj filmler full izle|hd flm izle|hdf?lm ?zle|4k flim izle|hd izle|hd turkce dublaj izle|s?k?ysa yakala|hd film izle turkce dublaj|4k izle film|sonsuz s?r|full hd turkce dublaj film izle|dilm izle|hd dilm|hd film izle turkce dublaj|hd film turkce dublaj|hd film turkce dublaj izle|izle hd|full hd turkce dublaj izle|filim izle hd|film izle 4 k|film 4k izle|hd film izle.|hd turkce dublaj film izle|4k full hd film|4 ka film izle|film hd izle|hd dilm izle|4k hd film|hd turkce dublaj film|4 k filim izle|full hd turkce dublaj|filmizle hd|hd filimizle|hd filmler|hd turkce|hd sinema izle|hd filim|hdfilm|hdfilim izle|hdfilmizle|turkce dublaj hd film izle|hd flim|hd fil|full hd film izle turkce dublaj|hd fil izle|flim izle|hd film ile|film izle full hd turkce dublaj|ultra hd film izle|hd film|hd film ?zle|hd film ize|full izle|hd film.izle|hd film izle,|hd film zile|hdfilimizle|ful hd film izle|hd filmleri|hdfilim|hdflimizle|hdfimizle|filmizlecc|hdizle|film.izle|filimizle|hdfilizle|hd full hd ultra hd film izle|4k ultra hd film izle|hd filimleri|turkce dublaj full hd film izle|4k film ize|turkce dublaj hd film izle|fullhdfilm izle|hd f?l?m ?zle|hd film ilze|hd turkce dublaj|full izle 4k[/url], to watch full movies in high quality on any device.

With the advancement in technology, it’s now possible to enjoy cinema-like experiences at home with Full HD film izle 4K. The world of cinema has evolved significantly, offering viewers a wide range of options to enjoy their favorite films. From action-packed blockbusters to romantic comedies, every genre is now available in stunning Full HD . Moreover, The future of entertainment is undoubtedly linked to the quality and accessibility of Full HD film izle 4K.

Now, with Full HD film izle 4K, the bar has been set even higher. The impact of Full HD on the film industry cannot be overstated. It has changed the way movies are produced, distributed, and consumed . Additionally, the rise of streaming platforms has democratized access to Full HD films .

Benefits of Full HD Film Izle 4K

The high resolution and superior sound quality make every movie night feel like a trip to the cinema . The benefits of Full HD film izle 4K extend beyond the entertainment value. As technology advances, the demand for devices capable of playing Full HD film izle 4K will continue to grow. Furthermore, Documentary films and educational content in Full HD can provide a more engaging and effective learning experience .

As the demand for Full HD film izle 4K continues to rise, it is likely that we will see significant investments in this sector. The future of Full HD film izle 4K looks promising. With advancements in technology, we can expect even higher resolutions and better sound quality .

Accessibility of Full HD Film Izle 4K

With the proliferation of smartphones and high-speed internet, watching Full HD films is no longer a luxury . The ease of access to Full HD content has been a game-changer. With Full HD film izle 4K, the boundaries of time and space are virtually eliminated. Moreover, This democratization of access has been a key factor in the popularity of Full HD film izle 4K.

The impact of accessibility on the popularity of Full HD film izle 4K cannot be overstated . The role of technology in enhancing accessibility is crucial. Advancements in cloud computing, data storage, and internet speeds have all contributed to the widespread availability of Full HD film izle 4K .

Future of Full HD Film Izle 4K

As technology continues to advance, we can expect even higher resolutions, better sound quality, and more immersive viewing experiences . The potential for innovation in Full HD film izle 4K is vast. From personalized entertainment experiences to interactive films, the possibilities are endless . Additionally, the environmental impact of Full HD film izle 4K should also be considered .

The way we consume entertainment says a lot about our culture and values . Furthermore, As the quality and accessibility of Full HD content continue to improve, its potential as a tool for learning and personal development will become more evident.

Service rubber stamp maker online|stamp making online|rubber stamp online maker|stamp maker|online stamp maker|stamp maker online|stamp creator online|make a stamp online|make stamp online|online stamp design maker|make stamps online|stamps maker|online stamp creator|stamp online maker|stamp online maker free|stamp maker online free|create stamp online free|stamp creator online free|online stamp maker free|free online stamp maker|free stamp maker online|make stamp online free allows you to create and order stamps online.

The rubber stamp maker online is a revolutionary tool that allows users to create custom rubber stamps from the comfort of their own homes . The process of creating a rubber stamp online is straightforward and requires minimal effort users can simply upload their design or use a pre-made template to create their stamp . The rubber stamp maker online is a great resource for businesses and individuals who need to create custom stamps for their documents .

users can create and order their stamps from anywhere with an internet connection . users can choose from a variety of fonts, colors, and images to create their custom stamp . users can create their own custom stamps at a fraction of the cost of traditional methods .

How to Use a Rubber Stamp Maker Online

To use a rubber stamp maker online, users simply need to visit the website and follow the instructions . The first step in using a rubber stamp maker online is to choose a design or template . they will be asked to provide their contact and payment information .

users can choose from different shapes, sizes, and materials . the tools include features such as text editing and image uploading. the website is easy to navigate and provides clear instructions.

Benefits of Using a Rubber Stamp Maker Online

users can create and order their custom stamps from anywhere with an internet connection . The online rubber stamp maker also offers a wide range of design options and templates . it reduces the need for physical stores and minimizes waste .

this can help to establish their brand and create a professional image. users can use these tools to promote their business and increase their online presence . the team is available to answer questions and provide guidance.

Conclusion

In conclusion, the rubber stamp maker online is a revolutionary tool that allows users to create custom rubber stamps from the comfort of their own homes . the possibilities are endless when it comes to designing custom rubber stamps online. the website is easy to navigate and provides clear instructions.

users can create their own custom stamps at a fraction of the cost of traditional methods . users can choose from a variety of fonts, colors, and images to create their custom stamp . users can create and order their custom stamps from anywhere with an internet connection.

Bakmak film izle hd.

Full HD film izlemenin keyifli yolları. Günümüzde, film izleme deneyimi büyük bir değişim geçirdi. Full HD ve 4K, izleyicilere farklı deneyimler sunar. 4K ise daha da yüksek çözünürlük ile görsel bir şölen yaratır.

Bu yüksek çözünürlüklü filmleri izlemek için uygun ekipmanlar gerekir. Yüksek çözünürlükteki görüntü kalitesi, kullanıcıları etkileyecektir. Full HD formatı, halen birçok izleyici için idealdir. Her film sever, kendi tercihine göre kalite seviyesini seçebilir.

Günümüzde pek çok film izleme platformu bulunmaktadır. Film severler, çeşitli platformlarda istedikleri filmleri bulabiliyor. Bu platformlarda, geniş bir film yelpazesi sunulmaktadır. Film seçme süreci, kişisel tercihlere bağlıdır.

Film izlemek, hayatımızın önemli bir eğlence kaynağı haline geldi. Full HD ve 4K, izleyicilere farklı tatlar sunar. Dolayısıyla, film izlerken tercihlerinizi belirlemek önemlidir. Sinema dünyasının tadını çıkararak, yeni filmleri keşfetmek için hazır olun.